Piercing the Corporate Veil: When Founders Lose Their Liability Shield

When entrepreneurs form a corporation or limited liability company (LLC), they often assume their personal assets are automatically protected from business debts and lawsuits. However, the limited liability provided by corporate formalities is not absolute, and it is important to be aware of certain circumstances when courts could “pierce the corporate veil” and make founders personally liable for corporate obligations.

What Is the Corporate Veil?

The corporate veil is a metaphorical barrier that protects shareholders (or members in an LLC) from personal liability for the actions and debts of their business. As long as the business is properly formed and maintained, creditors can only pursue the business’s assets – not the personal bank accounts, homes, or other property of the founders or investors.

Piercing the Veil: The Exception to the Rule

Piercing the corporate veil is a legal remedy used when the court determines that the company is not truly operating as a separate entity, but rather as an alter ego of its owners. Courts are generally reluctant to hold business owners liable for their company’s debts, but will do so in cases involving fraud, abuse, or failure to follow corporate formalities. The rationale is simple: the legal protections of incorporation should not be used to perpetrate injustice or evade the law.

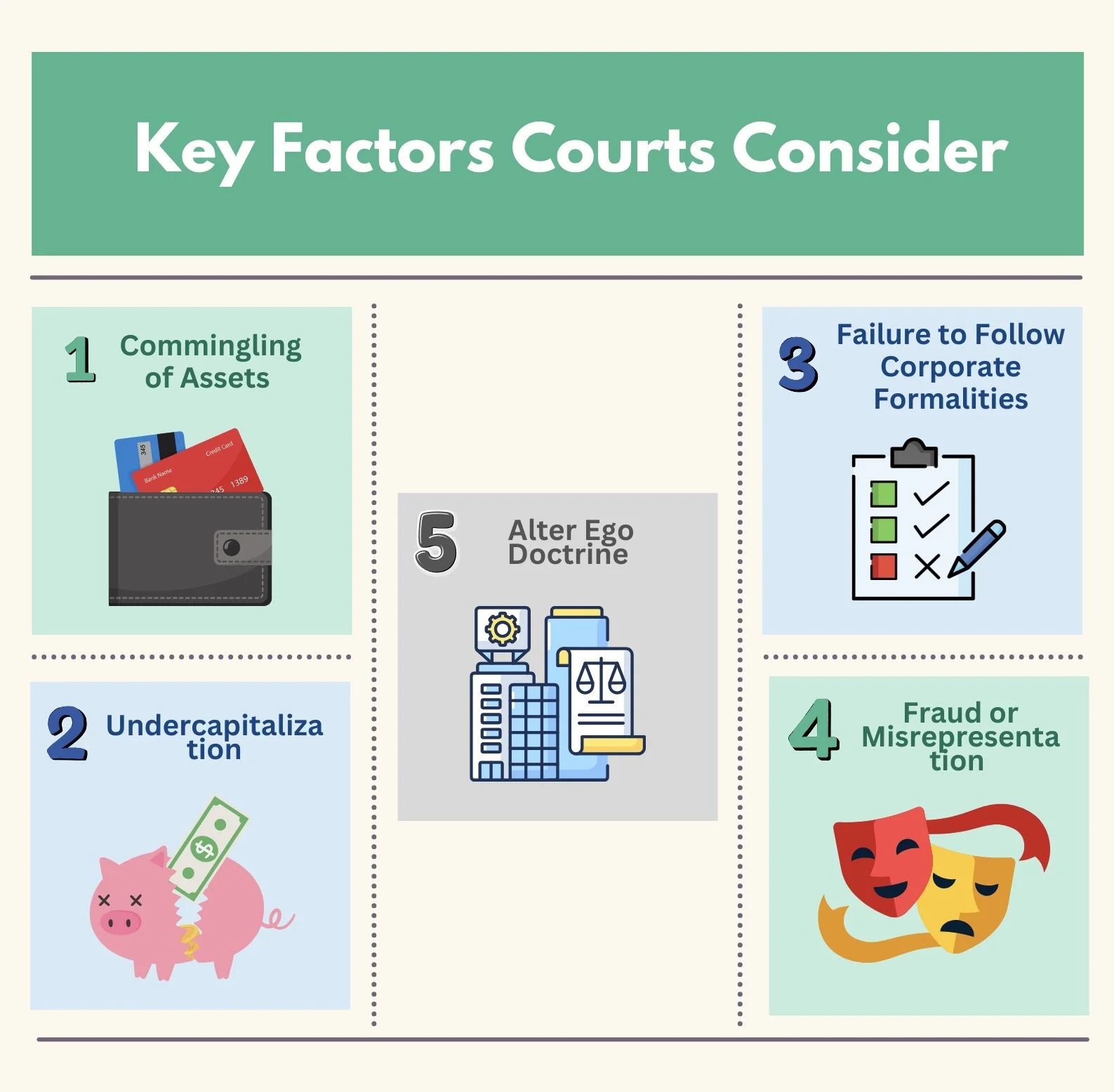

Common Factors Courts Consider

While the exact legal test varies by jurisdiction, most courts look for a combination of the following factors:

1. Commingling of Assets

Using business funds to pay personal expenses, or vice versa, is a red flag. If there is no clear distinction between personal and business finances, courts may conclude the business is merely a shell.

2. Undercapitalization

If a business is underfunded at the outset, making it unlikely to meet its liabilities, courts may view this as an intentional ploy to avoid corporate liability.

3. Failure to Follow Corporate Formalities

For corporations, this includes holding regular board meetings, maintaining minutes, and filing required documents. LLCs may have fewer formalities, but should still have a clear operating agreement and proper records.

4. Fraud or Misrepresentation

Using the corporate structure to deceive creditors, investors, or the public – whether through false statements or concealment – can justify piercing the veil.

5. Alter Ego Doctrine

If the owner exercises complete control over the company such that there is no meaningful separation between the individual and the business, the court may find the company is merely the "alter ego" of its owner.

Courts look for warning signs that a business is not truly separate from its owners

How Founders Can Protect Themselves

To avoid the risk of veil-piercing, founders should:

Maintain separate bank accounts for business and personal use.

Adequately capitalize the business at the outset.

Keep detailed records of business decisions and transactions.

Avoid personal guarantees unless absolutely necessary.

Follow all state filing requirements and corporate formalities.

Simple steps founders can take to keep their personal assets shielded.

Conclusion

Piercing the corporate veil is a legal remedy of last resort, but one that founders must take seriously. The best protection is proactive compliance: treat your business as a truly separate entity and avoid actions that might be perceived as deceptive or negligent. The corporate veil is not an absolute protection, and business owners can unwittingly expose themselves to personal liability they thought they had avoided if they fail to take adequate precautions.