The $1 Billion Earnout: J&J v. Fortis Advisors and the Limits of Buyer Discretion

When J&J acquired Auris Health, a medical robotics company, in 2019, it agreed to pay $3.4 billion upfront plus up to $2.35 billion in earnouts tied to regulatory milestones. None of the milestones were achieved. The seller's representative sued, alleging that the buyer had sabotaged the earnout rather than working to achieve it. After a ten-day trial, the Court of Chancery awarded over $1 billion in damages.

In Johnson & Johnson v. Fortis Advisors LLC, decided January 12, 2026, the Delaware Supreme Court largely affirmed. The court reversed on one issue (the implied covenant could not rewrite an express contract term), but upheld the breach of contract findings, the fraud verdict, and the bulk of the damages award.

The case offers three lessons for anyone negotiating or litigating earnouts. First, "commercially reasonable efforts" means what it says, and a buyer cannot deprioritize earnout milestones while claiming business judgment discretion. Second, the implied covenant of good faith cannot supply terms the parties could have negotiated but didn't. Third, an exclusive remedy clause will not shield a buyer from fraud claims based on extra-contractual statements unless the seller has clearly disclaimed reliance on those statements.

The Deal

Auris developed two robotic surgical platforms: Monarch, a lung-focused system that had already received FDA clearance, and iPlatform, a general-surgery robot designed to compete with Intuitive's da Vinci. The buyer viewed Auris as a solution to a problem. Its internal robotics program, Verb, was struggling, and surgical robots had become an "existential threat" to the buyer's instrument business as hospitals increasingly purchased Intuitive-branded tools instead of traditional Ethicon products.

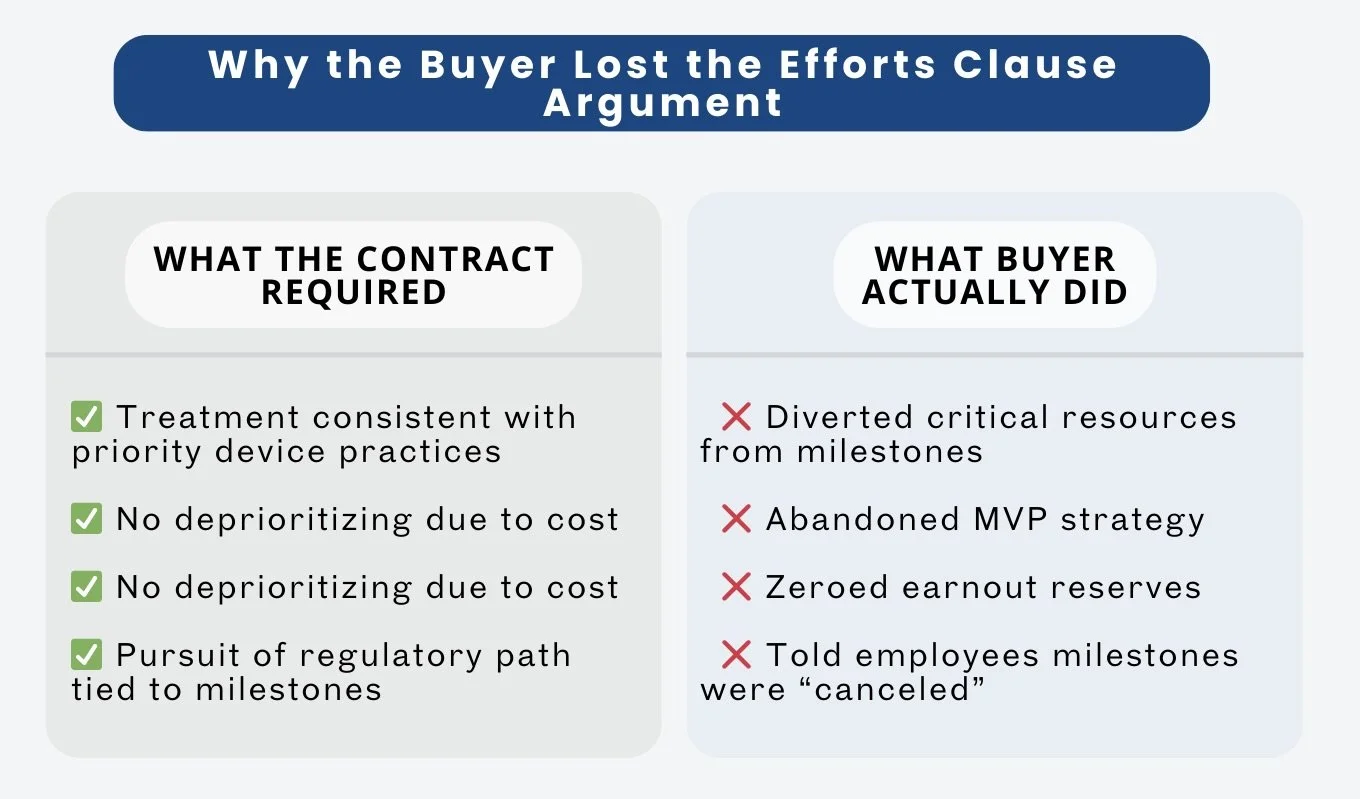

The merger agreement structured the purchase price as $3.4 billion upfront plus contingent payments tied to ten milestones, eight regulatory and two sales-based. The regulatory milestones were tied specifically to "510(k) premarket notification," the FDA's faster approval pathway for devices substantially equivalent to existing products. The agreement required the buyer to use "commercially reasonable efforts" to achieve the milestones, defined by reference to the buyer's "usual practice" for "priority medical device products of similar commercial potential."

The agreement also prohibited the buyer from taking any action "with the intention of avoiding" an earnout payment or "based on taking into account the cost" of making an earnout payment.

To induce the deal, the buyer's CEO told the seller's founder that one milestone, a $100 million payment tied to lung tissue ablation, was so "highly certain" that the buyer treated it as "effective up front" consideration. What the CEO did not disclose was that a patient in a related clinical study had recently died and the FDA had opened an investigation, putting the milestone's achievability in serious doubt.

What Happened After Closing

Within days of closing, the buyer launched "Project Manhattan," an internal competition pitting iPlatform against its struggling Verb robot. The exercise diverted more than 80 engineers from iPlatform's development roadmap, forced the team to prepare a prototype for complex procedures far beyond the initial milestones, and generated what the court described as "significant technical debt" that drove the program "backwards rather than forwards."

iPlatform won the bakeoff. But instead of treating it as a priority device, the buyer merged iPlatform with Verb, flooding the iPlatform team with over 200 Verb employees. The integration was, in the court's words, "a calamity of excess and redundancy." Within a year, every engineer from the legacy iPlatform clinical engineering team had left. The combined project fell behind schedule.

The buyer also abandoned the regulatory strategy that the milestones contemplated. The earnouts were structured around a "minimum viable product" approach: obtain clearance for simpler procedures first, then build to more complex surgeries. The buyer instead insisted on pursuing a complex procedure for the first milestone, even though it acknowledged internally that this approach would delay the timeline.

When the FDA shifted iPlatform from the 510(k) pathway to the more rigorous De Novo pathway, the buyer treated this as an excuse to abandon the milestones entirely. It wrote down the earnout reserves to zero, recording an immediate accounting gain of nearly $1 billion. It changed the employee incentive structure to remove any bonus tied to the contractual milestones. Internal communications told employees that the milestones had been "canceled."

By the end of 2021, the buyer pulled the plug on iPlatform. None of the $2.35 billion in earnouts was paid.

The Court's Analysis

The Delaware Supreme Court addressed three issues: the implied covenant, the breach of contract claims, and the fraud finding.

The Implied Covenant. The Court of Chancery had invoked the implied covenant of good faith and fair dealing to address the FDA's pathway change. Because the milestones specified 510(k) clearance and the FDA had required De Novo review instead, the lower court held that the implied covenant required the buyer to pursue De Novo approval as a functional substitute.

The Supreme Court reversed on this point. The implied covenant is a "limited and extraordinary remedy" that fills genuine gaps in a contract. It cannot rewrite express terms. Here, the parties had tied every regulatory milestone to "510(k) premarket notification" eight times over. They had acknowledged in the contract that FDA "developments" might affect the route, timing, or cost of approval. They could have drafted the milestones to include alternative pathways but chose not to. The risk that the FDA would require a different pathway was foreseeable, and the contract allocated that risk to the seller.

The court applied the principle from Nemec v. Shrader: the implied covenant addresses developments that "could not be anticipated," not developments that the parties "simply failed to consider." Because the regulatory shift was foreseeable and the contract was not silent on the pathway question, there was no gap for the covenant to fill.

This ruling eliminated damages for the first milestone ($400 million at a 75% probability, or $300 million). The remaining milestones, however, were unaffected. Once the buyer obtained De Novo approval for an initial indication, that approval could serve as the predicate for 510(k) submissions on subsequent indications. The buyer's express obligations under the efforts clause continued to apply.

Breach of the Efforts Clause. The Supreme Court affirmed the lower court's interpretation of the "commercially reasonable efforts" provision. The agreement required efforts "consistent with the usual practice of [the buyer] with respect to priority medical device products." The buyer argued that ten enumerated factors (safety, profitability, competitive positioning, and so on) gave it discretion to deprioritize the milestones whenever business considerations pointed elsewhere.

Buyer conduct fell far below the required effort standard.

The court rejected that reading. The ten factors permitted the buyer to calibrate its efforts within the "priority device" baseline, not to override that baseline entirely. A construction that allowed the buyer to invoke profitability or competitive concerns to justify abandoning the milestones would render the "priority medical device" language superfluous. It would also nullify the provision prohibiting the buyer from acting "with the intention of avoiding" the earnouts.

The court noted that the buyer's treatment of iPlatform diverged sharply from its treatment of Velys, its own priority orthopedic robot. Velys was not subjected to a bakeoff, forced to integrate with another program, or stripped of milestone-based incentives. Under the contract, iPlatform should have received comparable treatment.

Fraud. The Supreme Court also affirmed the fraud finding. The CEO's statement that the lung ablation milestone was "highly certain" and "effective up front" consideration was made ten days after the deal team had been briefed on a patient death and FDA investigation that put the milestone in serious jeopardy. The court held that presenting the milestone as essentially guaranteed while concealing material information about its achievability constituted active concealment.

The buyer argued that its exclusive remedy clause barred post-closing fraud claims. The court disagreed. Under Abry Partners, a party cannot escape liability for fraud based on extra-contractual statements unless the counterparty has clearly disclaimed reliance on such statements. The merger agreement contained an anti-reliance clause, but it ran only against the buyer. The seller never disclaimed reliance on extra-contractual representations. Absent that disclaimer, the exclusive remedy clause could not bar the seller's fraud claim.

Practical Implications

For sellers negotiating earnouts: Tie the buyer's “efforts” obligation to an internal benchmark the buyer actually cares about. This deal used "priority medical device products," which gave the seller a concrete comparator (Velys) for measuring the buyer's performance. Generic "commercially reasonable efforts" language would have been far easier for the buyer to satisfy.

Consider what happens if regulatory pathways change. If the milestones depend on a specific approval route, specify what happens if that route becomes unavailable. The seller here could have included language requiring the buyer to pursue alternative pathways or adjusting the milestones if the FDA changed course. It didn't, and the court refused to imply such terms.

Get oral assurances in writing. The CEO's statement about the lung ablation milestone being "highly certain" helped establish fraud, but fraud claims are expensive and uncertain. Better to capture material assurances as contractual representations backed by indemnification.

For buyers structuring earnouts: The ten factors in this agreement were supposed to preserve buyer discretion. They didn't work as intended because the court read them as operating within the "priority device" requirement, not as overriding it. If you want meaningful discretion to deprioritize earnout-related programs, the contract needs to say so explicitly and cannot simultaneously promise "priority" treatment.

Do not treat earnouts as optional. The buyer here wrote down the milestones to zero, removed them from employee incentive plans, and told employees the milestones were "canceled." This conduct made the breach findings easy. If you commit to use commercially reasonable efforts to achieve milestones, you need to actually pursue them, even if business circumstances change.

Anti-reliance clauses should run both ways. The buyer had the seller disclaim reliance on extra-contractual statements, but the seller never made the same disclaimer. That asymmetry left the buyer exposed to fraud claims based on its CEO's oral assurances during negotiations.

For deal lawyers generally: Earnout provisions with efforts obligations are not self-executing. They require careful drafting of both the milestone conditions and the efforts standard, attention to what happens when circumstances change, and clear allocation of discretion between the parties. This case shows what happens when a sophisticated buyer assumes it can exercise judgment post-closing that the contract does not actually permit.

The Takeaway

The buyer paid $3.4 billion for Auris and will now pay approximately $700 million more in damages (the original $1 billion award minus the reversed Milestone 1 damages). It also generated the legal fees and management distraction of a ten-day trial and an appeal to the Delaware Supreme Court.

The earnout structure was supposed to bridge a valuation gap. Instead, it created a seven-year dispute that cost both sides enormously. The seller would have been better off with less contingent consideration and more upfront cash. The buyer would have been better off honoring its commitments or never making them in the first place.

The lesson is not that earnouts are unworkable. It's that they require the buyer to actually pursue the milestones with the promised level of effort. If the buyer doesn't intend to do that, it shouldn't agree to the provision. And if it does agree, it should assume a Delaware court will hold it to what it promised.