The Term Sheet Handshake: Red Flags Every Founder Must Spot Before Signing

A term sheet is not a contract. It’s a handshake. But you can learn a lot about a person by how they shake your hand.

Investors are on their best behavior during term sheet negotiations. They want the deal. They're courting you. If you're seeing red flags now, imagine what happens when the company hits a rough patch and their capital is on the line.

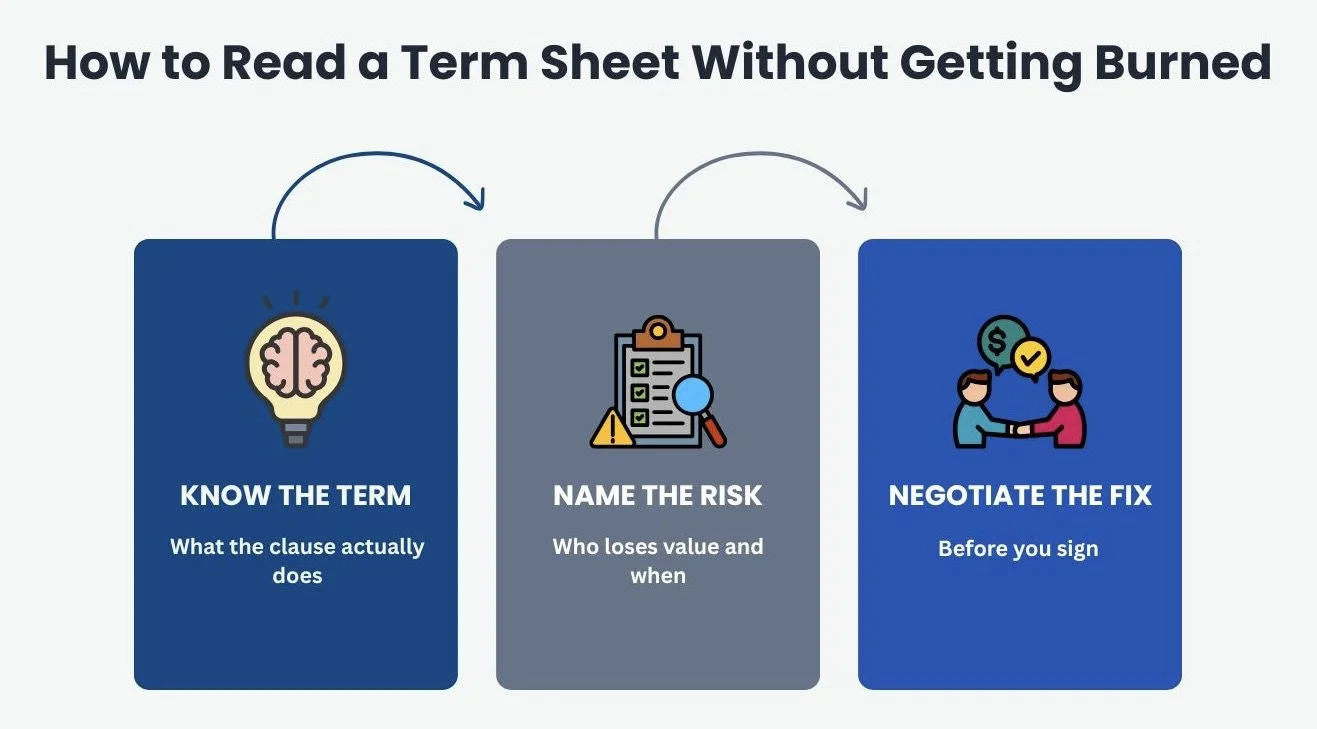

This post is a guide to the provisions that should make you pause, ask questions, or walk away. The framework is simple: know the term, name the risk, negotiate the fix.

What’s a Term Sheet?

A term sheet outlines the key economic and governance terms of an investment. It is typically non-binding, except for a few provisions like confidentiality and exclusivity. The binding details come later in the definitive documents: the stock purchase agreement, investor rights agreement, voting agreement, and certificate of incorporation.

But here's the thing. Once you sign a term sheet, you've largely set the terms. Renegotiating after signing is difficult, awkward, and signals that you didn't understand what you agreed to. The definitive documents will be drafted by the investor's lawyers based on the term sheet, and pushing back at that stage creates friction.

The time to negotiate is before you sign. Which means the time to spot problems is now.

Understand the term. Identify the risk. Negotiate early.

The Red Flags

For each of these, you need to understand what's standard, what's aggressive, and what's a walk-away.

Participating Preferred Stock

Preferred stock comes in two flavors: non-participating and participating.

With non-participating preferred, the investor chooses between getting their liquidation preference back or converting to common stock and sharing pro rata in the proceeds. They pick whichever is better. This is standard and fair.

With participating preferred, the investor gets their liquidation preference back and then also converts to common and shares in the remaining proceeds. They double-dip.

Participating preferred significantly reduces what founders and employees receive in an exit. It matters most in modest outcomes. If you raise $5 million on a $20 million post-money valuation with participating preferred, and the company sells for $25 million, your investors don't just get their money back or their 25% ownership stake. They get $5 million off the top, then 25% of the remaining $20 million. That's $10 million to them, $15 million to everyone else. With non-participating preferred, they'd choose conversion and take $6.25 million, leaving $18.75 million for everyone else.

If an investor insists on participation, negotiate a cap. A 3x cap stops the double-dip after three turns. Not ideal, but it limits the damage.

Liquidation Preferences Above 1x

A 1x non-participating liquidation preference is standard. The investor gets their money back before common stockholders receive anything. This makes sense; they took the risk of investing, and they deserve downside protection.

Preferences above 1x are a different story. A 2x preference means the investor gets twice their investment back before you see a dollar. A 3x preference means three times. These multiples can turn a decent exit into a wipeout for founders and employees.

High liquidation preferences often signal that the investor is worried about overpaying or expects the company may not hit its targets. Neither is a good sign. If you see 2x or 3x, ask why. If the rationale is fuzzy, change the money, not your future.

Full Ratchet Anti-Dilution

Anti-dilution provisions protect investors if you raise a future round at a lower valuation. There are two main types: weighted average and full ratchet.

Weighted average anti-dilution adjusts the investor's conversion price based on the size and price of the down round relative to the prior round. It's a proportional adjustment. This is standard and reasonable.

Full ratchet anti-dilution reprices the investor's shares to the new lower price, regardless of how small the down round is. If you raised at $10 per share and later raise a small bridge round at $5 per share, full ratchet reprices all of the earlier investor's shares to $5. The dilution to founders and employees is brutal.

Full ratchet is rare in healthy markets and almost always a red flag. It signals either an unsophisticated investor or one extracting terms because they have leverage. Either way, the handshake is telling you something. Listen.

Founder Vesting Resets

You've already been working on this company for two years. You have a standard four-year vesting schedule that's half complete. Then the term sheet says all founder shares will be subject to a new four-year vesting schedule starting at closing.

This is a vesting reset, and it's a significant economic hit. You're giving back two years of vesting you've already earned.

Some acceleration of unvested shares for founders is reasonable in connection with new investment. But a complete restart is aggressive. If an investor proposes this, understand their rationale. Sometimes it reflects legitimate concern that a founder might leave post-funding. More often it's a leverage play.

Push back; at minimum, credit time served. If they won't, ask yourself whether you're choosing a partner or a boss.

Board Control

Early-stage term sheets often propose a three-person board: one founder seat, one investor seat, one independent. That's balanced. As you raise more money, boards grow, but founders typically retain control or parity through Series A and often Series B.

Watch for term sheets that give investors board control from day one. Two of three seats. Three of five. This handshake comes with a tighter grip than you want.

Investors with board control can fire you, block strategic decisions, and force outcomes you don't want. They may never use that power. But they have it and it could mean all the difference in a dispute.

Related: pay attention to protective provisions. These are veto rights over major company actions. Raising money. Selling the company. Taking on debt. Changing the charter. Some protective provisions are standard. But an expansive list gives investors functional control even without board seats.

Read the protective provisions carefully. If you need investor consent to hire key employees, change your business model, or spend above modest thresholds, you're not running the company. You're managing it for someone else.

Redemption Rights

Redemption rights allow investors to force the company to buy back their shares after a specified period, usually five to seven years. In theory, this gives investors an exit if the company hasn't gone public or been acquired.

In practice, redemption rights create a ticking time bomb. Most startups don't have the cash to redeem investor shares. If redemption is triggered and you can't pay, you're in default. That default can give investors leverage to force a sale, replace management, or extract other concessions.

Redemption rights are more common in later-stage deals and with certain investor profiles: some corporate VCs, international investors. They're less common in early-stage deals with traditional venture firms. If you see them, understand exactly what triggers redemption and what happens if you can't pay. A friendly handshake today can become a chokehold in year six.

Cumulative Dividends

Most preferred stock has a stated dividend rate, often 6-8% annually. In standard deals, these dividends are non-cumulative, meaning they only get paid if and when the board declares them. Boards almost never declare dividends in venture-backed startups, so this provision has no practical effect.

Cumulative dividends are different. They accrue whether declared or not, and they add to the liquidation preference over time. After seven years, an 8% cumulative dividend has added more than 50% to what investors get paid before common stockholders see anything.

Cumulative dividends quietly erode founder and employee value. The handshake looks the same on day one; the grip tightens every quarter. Negotiate them out or convert them to non-cumulative.

Super Pro-Rata Rights

Pro-rata rights let existing investors maintain their ownership percentage by participating in future rounds. This is standard and generally founder-friendly; it keeps your current investors engaged.

Super pro-rata rights let investors increase their ownership percentage in future rounds, often up to 2x or 3x their current stake. This can crowd out new investors and make future fundraising harder. New lead investors want meaningful ownership; if your existing investors are taking a huge chunk of the round, the new investor's allocation shrinks.

Super pro-rata can also signal that the current investor wants to control your cap table, which creates its own issues. Standard pro-rata is fine. Anything more deserves a hard look.

Aggressive No-Shop Provisions

Term sheets typically include a no-shop clause preventing you from soliciting other offers during a defined period, usually 30-60 days. This protects the investor while they conduct due diligence and draft documents. Reasonable and standard.

Watch for no-shop periods that are too long, that extend automatically, or that survive termination of the term sheet. Some require you to disclose any inbound interest to the investor, giving them a right to match. These provisions reduce your leverage and can trap you in a deteriorating deal.

Keep it short, keep it clean, kill auto-extends.

Unclear or Missing Terms

Sometimes the biggest red flag is what isn't in the term sheet.

A term sheet that's vague on key economics, that says "to be determined" on important governance provisions, or that omits standard founder protections is inviting a fight later. The investor's lawyers will draft definitive documents that fill in those blanks, and they won't fill them in your favor.

If it matters, write it. If they resist writing it, they'll resist living it.

How to Use This Information

Spotting a red flag doesn't mean you should walk away. It means you should ask questions.

Why is the investor proposing participating preferred? Is it their standard term, or a reaction to something specific about your deal? Are they willing to negotiate? If you push back, do they engage constructively or dig in?

The negotiation process itself is information. Investors who are rigid on aggressive terms during courtship will be difficult partners when things get hard. Investors who explain their reasoning and negotiate in good faith signal how they'll behave as board members and allies. The handshake tells you about the relationship to come.

Use your lawyer. A good startup lawyer has seen hundreds of term sheets and knows which terms are standard, which are aggressive, and which are genuine dealbreakers. They can also help you negotiate without poisoning the relationship. That's what you're paying them for.

Practical Takeaways

For founders: not all money is equal. The terms attached to an investment determine whether that capital helps you build a company or slowly transfers value from you and your team to your investors. Don't sign a term sheet you don't understand. Don't assume bad terms will work themselves out later. Don't let the excitement of a funding round cloud your judgment.

For investors: aggressive terms may win you deals in the short run, but they create misaligned incentives and resentful founders. The best returns come from partnerships where everyone is pulling in the same direction. Structure your deals accordingly.

For lawyers advising founders: your job isn't just to redline documents. It's to help your client understand what they're signing and why it matters. Translate legalese into business impact. Flag the issues that will hurt them in three years, not just the ones that look bad today.

A term sheet is a handshake. Make sure you know whose hand you're shaking, how tight they intend to grip, and whether they plan to let go.