The Co-Founder Breakup Playbook: Legal Steps When a Business Partnership Ends

Every co-founder relationship begins with optimism. Shared vision, complementary skills, late nights fueled by the conviction that you're building something great. Nobody thinks about the exit when they're drafting the pitch deck.

Then something changes. The vision diverges. Trust erodes. And suddenly you're sitting across from someone you once considered family, trying to figure out how to unwind a business relationship without destroying the business itself.

I've guided dozens of founders through this process. The ones who come out intact share a few things in common: they moved deliberately, they separated emotion from economics, and they had a plan. This post is about that plan.

Why Co-Founder Breakups Are So Hard

A co-founder separation has all the emotional intensity of a divorce with all the financial complexity of an M&A transaction. You're unwinding a relationship built on trust while negotiating asset division with someone you may no longer trust at all.

The stakes are high. Get it wrong, and you blow up the company, trigger investor panic, lose key employees, or end up in litigation that drains resources for years. Get it right, and one founder exits cleanly while the other keeps building.

The difference between those outcomes usually isn't the underlying facts. It's how the separation is handled.

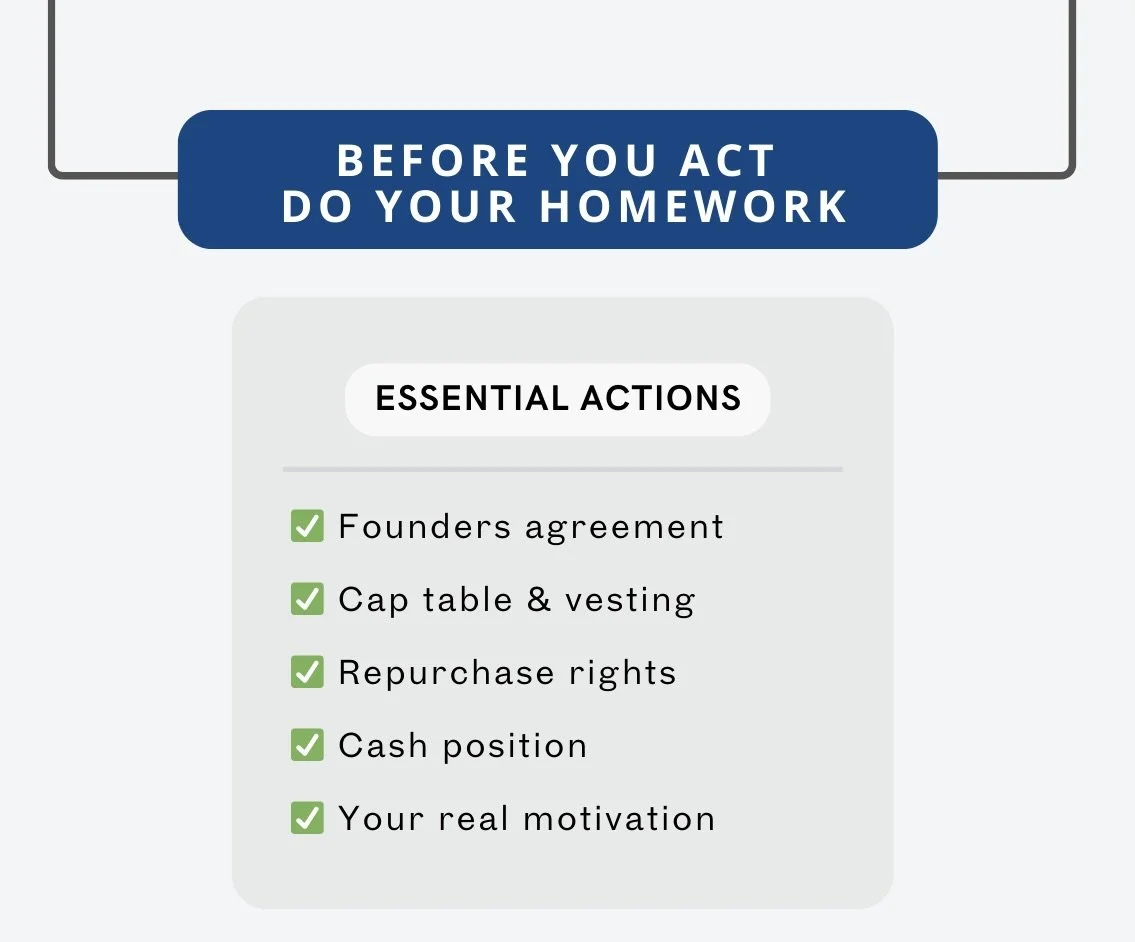

Before You Do Anything: Assess the Situation

A co-founder breakup should start with preparation, not confrontation.

When a co-founder relationship fractures, the instinct is to act. Confront the problem. Force a resolution. Have the difficult conversation.

Resist that instinct until you've done your homework. In a divorce, you wouldn't negotiate custody without knowing what the prenup says. Same principle here.

Start with the documents. Pull your founders' agreement, stock purchase agreements, vesting schedules, certificate of incorporation, bylaws or operating agreement, and investor agreements. The answers to most of your questions are in there.

Key questions: What does each founder own, and how much is vested? Are there acceleration provisions triggered by departure? Does the company have repurchase rights or a right of first refusal? Are there provisions addressing founder disputes or deadlock? What do investor agreements require?

Then assess the practical realities. Who does what? What happens to those functions if one founder leaves? What's the company's cash position?

Finally, check your own motivations. Are you trying to solve a problem or win a fight?

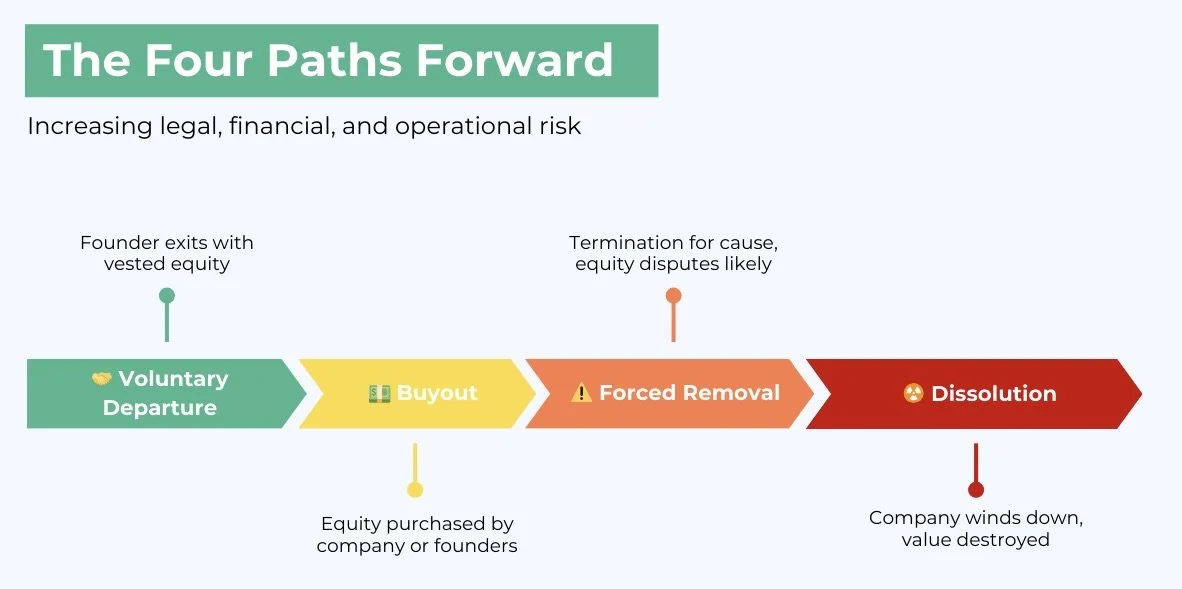

The Four Paths Forward

Not all co-founder breakups are equal. Understanding the available paths helps founders choose the least destructive outcome.

Co-founder separations follow one of four paths. Think of them as settlement options, ranging from amicable to nuclear.

Path one: Voluntary departure with equity retention. The departing founder leaves but keeps vested equity. This works when the separation is amicable and everyone is comfortable with a passive shareholder on the cap table. Simplest path, but requires trust.

Path two: Buyout. The company or remaining founders purchase the departing founder's equity. Clean break, but requires cash or structured payments. Common when the separation is less amicable or a former co-founder on the cap table complicates future fundraising.

Path three: Forced departure. The departing founder is terminated for cause, unvested shares forfeit, and vested shares may be repurchased at a reduced price. Most contentious path, often leads to disputes about whether cause existed.

Path four: Company dissolution. When founders can't agree on who leaves and can't work together, the only option may be winding down and dividing assets. Nuclear option. Destroys value. Avoid if possible.

Most separations land between paths one and two. The goal is an exit both parties can live with, not total victory. In divorce and in business, total victory usually means everyone lost.

The Buyout Mechanics

If you're heading toward a buyout, this is where the M&A complexity kicks in.

Valuation. What's the equity worth? Early-stage companies are hard to value. Common approaches: most recent fundraising valuation, a formula based on revenue, independent appraisal, or a negotiated number. If your founders' agreement specifies a method, start there.

Payment terms. Lump sum or installments? Most startups can't write a large check, so buyouts are often structured over time, sometimes contingent on milestones or a future exit. Departing founder wants security; company wants flexibility. Find the middle.

Vested vs. unvested. Unvested shares typically forfeit. Vested shares are trickier. The departing founder owns them, but repurchase rights may apply. Check the price formula and whether it varies based on voluntary departure versus termination for cause.

Acceleration. Some agreements accelerate unvested equity on termination without cause or change of control. Know your terms before negotiating.

Every buyout term is a tradeoff between certainty and flexibility. Structure the deal so both sides get enough of what they need to sign.

The IP Handoff

Intellectual property is often the company's most valuable asset. In M&A terms, it's the asset that makes the deal worth doing. Clouded title kills value.

If your assignment agreements are solid, the handoff is straightforward: all IP created for the company belongs to the company. But I've seen too many startups where the paperwork is incomplete. Founders never signed invention assignments. Core technology was built before formation and never transferred. Assignments exist but have gaps.

Before any founder exits, audit your IP chain of title. If there are gaps, the separation is your chance to fix them. Make clean assignment a condition of the buyout.

Also address ongoing obligations: confidentiality, non-compete, non-solicit. Know what your agreements say and what state law allows.

Investor Considerations

If you've raised capital, investors have a stake in how this unfolds. Think of them as the in-laws: not parties to the marriage, but deeply interested and capable of making things easier or harder.

Review investor agreements for required consents or notices. Some require approval for equity repurchases. Others require notification of material events.

Beyond legal requirements, think about relationships. Investors backed the team. A founder leaving raises questions. Handle it poorly, and you shake confidence. Handle it well, and you demonstrate maturity.

Get ahead of the narrative. Brief lead investors early. Present a considered decision with a clear plan.

Structuring the Exit Agreement

If the negotiation is the divorce proceeding, the exit agreement is the decree. It governs everything.

Cover equity treatment, IP assignment, ongoing restrictions (confidentiality, non-compete, non-solicit, non-disparagement), mutual releases, transition obligations, and reps and warranties.

Don't shortcut this document. Every ambiguity is a future dispute. Every omitted term is a negotiation you'll have later, when the relationship is worse and leverage has shifted. Get it in writing, get it right, get it signed.

Managing the Transition

In a divorce, the kids are watching. In a startup, so are employees, investors, and the market.

Communicate with employees promptly. They're anxious about what this means for the company and their jobs. Uncertainty breeds rumors; rumors breed attrition.

Handle the departing founder with dignity, even if the relationship has soured. Everyone is taking notes.

Create a real transition plan. What transfers, to whom? What needs documenting? What relationships need introductions? A 30-day cooperation period means nothing if you don't use it.

When It Goes Wrong

Sometimes separations can't be negotiated. That's when the divorce goes to trial.

Preserve your documents. Emails, texts, Slack messages, board minutes. Destroying evidence, even unintentionally, is catastrophic.

Don't make admissions. Assume everything could become an exhibit.

Get litigation counsel early. Your corporate attorney may be excellent at transactions but less experienced in disputes.

Consider mediation before filing. Cheaper, faster, more confidential. Even bitter divorces sometimes settle on the courthouse steps.

Practical Takeaways

For founders facing a breakup: slow down, separate emotion from economics, and get counsel before you negotiate. The goal is a clean exit, not a scorched-earth victory.

For founders building new companies: this is why you need a founders' agreement with clear vesting, repurchase rights, and dispute resolution. A good prenup isn't pessimistic; it's practical.

For attorneys advising startups: founder disputes are where transactional planning meets litigation reality. The documents you draft today determine how separations unfold years later.

A co-founder breakup has the emotional weight of a divorce and the financial stakes of an M&A deal. But it doesn't have to end in scorched earth. With preparation, clear documentation, and professional guidance, one founder exits while the other keeps building. The company survives. The cap table stays clean. Everyone moves on.

Plan for it before you need it.