What Every Founder Should Know About Vesting Schedules

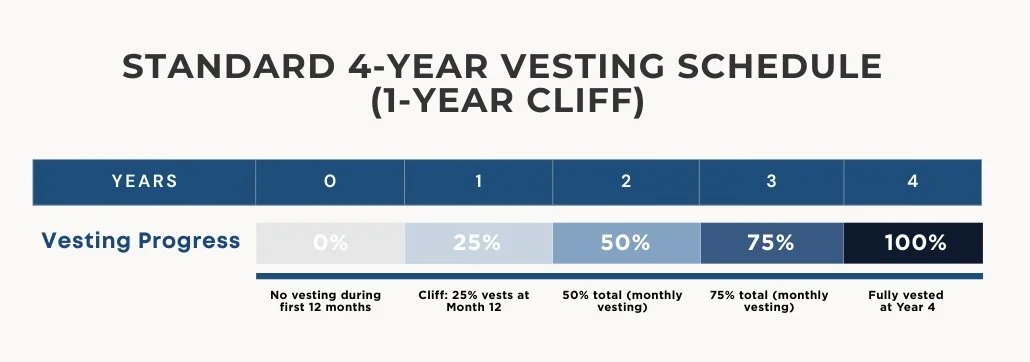

Vesting is a timetable for earning ownership. An incoming co-founder, for example, receives stock or options that vest over a stated period instead of all at once. A common schedule for startups is four years with a one-year cliff, which is a one-year minimum service period. Under this schedule, nothing vests during the first twelve months. At the one-year mark, a defined amount vests at once. After that, vesting continues monthly for the remaining three years.

Understanding how equity vests over time helps founders make smarter decisions about compensation, commitment, and long-term alignment.

The practical result is straightforward. If someone leaves early, the company does not lock in a long-term ownership stake for short-term work. If they stay, ownership accumulates predictably.

Why use vesting? Early teams change quickly. Roles evolve. People exit. Without vesting, a former contributor can keep a large, permanent share of the company, which complicates hiring, fundraising, and a future sale. With vesting, ownership follows contribution over time, preserving flexibility for the company and fairness for the team that remains.

A strong vesting policy helps maintain a clean cap table, which is essential for hiring, fundraising, and future growth.

When negotiating your vesting schedule, be intentional about the terms that fit your situation. A reduced cliff may be appropriate where the incoming stakeholder has already contributed. If a contractor effectively worked full-time for several months before joining, the company can credit those months. A founder who contributes a patent, a dataset, or a codebase can receive a small immediate grant and vest the balance. If it is properly documented, you can tailor the schedule to match the relationship.

Vesting Acceleration

Acceleration means unvested equity can vest ahead of schedule. It can be triggered by a single event or by a combination of events.

A common single-event example: if the company is sold, a defined portion of the unvested equity vests at closing.

A common two-event example: if the company is sold and you are terminated without cause, or pushed into a materially worse role within a defined window after closing, a defined portion vests at that point.

However you structure acceleration, it should never be a surprise. Negotiate the triggers, percentages, and timelines before you commit.

Renegotiating After a Change in Circumstances

Vesting should reflect the work ahead, not just the work behind. When roles shift, revisit the schedule. Common triggers include a co-founder moving to part-time, a senior hire taking an extended leave, a leader stepping into a different scope, or a contributor returning after a gap.

Keep the mechanics simple. Re-vest a defined portion of the unvested equity so it earns out over a new timetable, without touching what has already vested. Document the change through a written amendment that references the original grant, states the revised vesting start date for the re-vested portion, and updates any acceleration terms that depend on service time.

Guardrails help. Tie the re-vesting to concrete expectations, such as reduced hours for a set period, a transitional role with named deliverables, or a planned return date. If the arrangement is temporary, include a review date when the schedule will be restored or adjusted. Transparency prevents the quiet resentment that builds when titles and ownership drift in different directions.

Advisory Equity and Vesting

Advisory grants should be earned on a clock and tied to real work. Treat them as service compensation, not souvenirs. A practical pattern is a one- to two-year schedule with quarterly vesting, paired with deliverables such as monthly strategy sessions, introductions to named partners, or a project with defined outputs. If participation stops, vesting stops.

Put expectations in writing. An advisor letter should include the total grant, vesting schedule, meeting or project cadence, confidentiality, and IP assignment for work product. Clarify access boundaries, for example read-only data rooms or limited product sandboxes. State whether any acceleration applies in a sale. Many companies set advisor acceleration at zero so that sale economics favor the operating team.

Keep scope reasonable. Advisory equity should match actual involvement and company stage. Revisit only if the relationship deepens meaningfully, and then amend the agreement with fresh deliverables and a refreshed calendar. The result is a cap table that rewards real help and stays clean when interest fades.